Last month I published a newsletter explaining my bipartisan attitude toward retirement planning. If you haven’t read that, PLEASE DO SO NOW before continuing.

In that newsletter I posed the critical question: How will you create a financial strategy where you are going to be OK no matter what party is in office, no matter what interest rates are, no matter what happens in the stock market, no matter how volatile the times?

In this letter, I’m going provide a bit more context before answering that question. This is very important, because you must understand the problems in order to have any chance to solve them!

I am justifiably hard on the government, Wall Street, and generally, the “elites,” even labeling them as the problem. But why is that?

To be fair and honest, it’s not all their fault. Economies are immeasurably complex. So are global politics. So is the climate, among many other topics. Literally immeasurable. Our founding fathers recognized not only the complexity of the world (and it was simple then by comparison!), but also the nature of human beings, and that government was ill-equipped and should not be designed to intrude into our lives any more than necessary. The government was designed to provide for our common defense, to prevent one from infringing on another’s rights, to prevent itself from becoming too powerful, and to get out of the way.

We have strayed colossally from the original vision.

Now, economists and politicians struggle with the impossible task of measuring the unmeasurable, quantifying the unquantifiable, and then designing policy around it that can be spoon fed in 30-second increments to the most unsophisticated of people. And financial brokers, rather than designing policy, sell investments so you can make bets on these incomprehensible factors with your retirement plans.

The results? In 246 years of nationhood we still haven’t mastered running a postal service, yet we have the naïveté or the hubris to attempt to control global markets. Our track record shows that despite all of the meddling and all the money we throw at our institutions – whether in education, the medical system, or the environment – we can’t seem to solve the problems. In fact, we generally make them worse and ourselves poorer in the process, continuously mortgaging away our future.

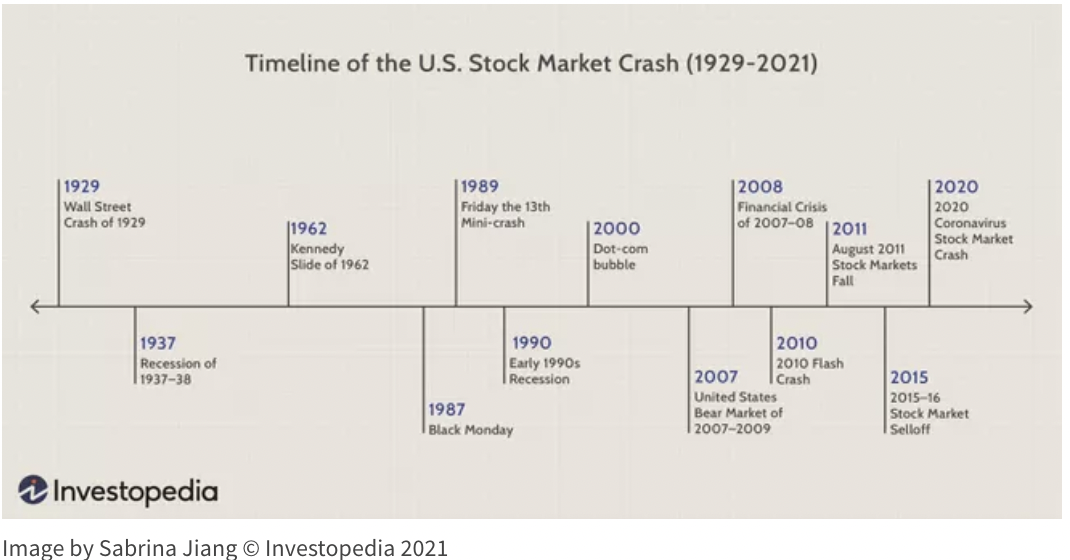

This arrangement inevitably has created uncertainty, volatility, booms and BUSTS. Ask yourself if this is true! Do we have more stock market crashes now than 40 years ago, or less? Compared to the past, are company values (and stock prices) driven more by their business fundamentals and products, or are their values increasingly affected by factors beyond their control like interest rates, pandemics, politics and other crises?

Is your retirement outcome more about saving and skill, or factors beyond your control? If so, why are you OK with that?

What if you could have the house’s odds instead of the players’? If you had to make a bet, would it be a better bet that Black Swans will not happen, or that they will? Would you rather be hurt by Black Swan events or take advantage of them? If you ask the right questions, the answers are easy.

As an alternative to playing the stock market casino with your retirement security, and instead of depending on the government to take care of you, you can grow your money safely and efficiently, in a tax-free manner, and not participate in the losses associated with crashes, uncertainty and volatility. At the same time, you can access your money any time you want, for any thing you want, without affecting or interrupting the growth of the original asset.

In short, you can be in control. See you next time.

Contact us for a free 15-minute phone consultation.

Thank you for your time and for taking control of your financial future!

Sincerely,

Sam Arieff

Arieff Consulting

(904) 478-0102

* Dividends are not guaranteed. However, companies we use have paid dividends without fair for more than 100 consecutive years.

Disclaimer: This newsletter represents the opinion of Arieff Consulting, Inc, and does not constitute financial, tax, or legal advice.